Amidst the uncertainties and challenges facing future global trade, it is essential not to overlook the potential consequences of economic decoupling if the geopolitical rivalry between China and the United States escalates further. Thus, understanding these dynamics and preparing for their implications will be key to maintaining stability and promoting growth in the evolving global trade system.

The growth of international trade and the expansion of global value chains (GVCs) over the past three decades have produced remarkable developmental effects. Incomes have surged, productivity has soared—particularly in developing nations—and poverty rates have plummeted. The intensification of production and the transfer of knowledge inherent in GVCs have played a pivotal role in driving these advancements. The heightened specialization of firms at various stages of value chains has bolstered efficiency and productivity, while enduring firm-to-firm relationships have facilitated technology transfer and provided access to capital and inputs along value chains. Presently, GVCs account for approximately half of world trade. However, there is cause for concern regarding the sustainability of this trade-driven path to development. Conflicts, disruptions of trade routes, and trade wars between superpowers threaten to undermine these gains. Despite a rebound in trade following the COVID-19 crisis, the robust growth rates witnessed in the 1990s and 2000s have proven elusive. (1)

The potential for trade conflicts among major nations, particularly, between the United States and China threatens to trigger a retrenchment or fragmentation of GVCs. Therefore, unlocking the developmental potential of GVCs in the present context demands proactive policies and the implementation of strategies to mitigate risks associated with trade tensions and disruptions. The implications for future trade in the era of GVCs will undoubtedly reshape the landscape of global commerce. These changes pose challenges such as increased costs, supply chain disruptions, and policy uncertainty. Adapting to these shifts will be crucial for policymakers to navigate the complexities of the new trade environment effectively. Several critical questions need to be addressed: Is there still a viable path for development through GVCs amidst the backdrop of trade wars and rivalry? What is truly at stake in the U.S.-China trade relationship? How will global trade look in the future?

The rivalry between the United States and China appears deeply intertwined and mutually reinforcing. On the one hand, their geopolitical competition significantly shapes the framework of economic and trade policies. Conversely, their economic and trade policies often serve to redistribute power and wealth, thereby influencing the trajectory of their ongoing rivalry. Consequently, this dynamic gives rise to a new world order as the competition intensifies, leading to a transformation of the political landscape and the emergence of a new structure of trade relationships.

A shift in the distribution of wealth and power will inevitably lead to changes in the structure and operation of global trade. Without the emergence of another hegemon capable of upholding openness, the system is prone to becoming more closed as states adopt increasingly nationalistic policies. This may involve the imposition of tariffs, restrictions on foreign investment, and limitations on the export of technology in an attempt to gain or maintain advantages over one another. Thus, the future of trade hinges significantly on the trajectory of this rivalry, as it shapes the rules, norms, and institutions that govern international commerce.

Historically, the United States has championed free trade and globalization, advocating for open markets and liberal economic policies. However, the rise of China as a formidable economic power has challenged this status quo, leading to tensions over trade practices, intellectual property rights, and market access. This friction between the two economic giants has resulted in tit-for-tat retaliatory measures and the imposition of trade barriers. Moreover, the evolving trade tensions have given rise to a new trade lexicon that reflects these shifts, incorporating terms such as “fragmentation,” “deglobalization,” “reshoring,” “nearshoring,” “friend-shoring,” “de-risking,” “decoupling,” “open strategic autonomy,” and “new industrial policy.” These terms are increasingly prevalent in discussions surrounding trade policies between the world’s two largest economies. (2)

Threat to the Global Trade:

Concerns about the future of the global trading system and the potential outcome of an all-out trade war between China and the United States are escalating. Instead of leading to the reform and modernization of the current trading system, this competition could threaten its stability and lead to its collapse. Currently, the trading system focuses on two key areas for reform: firstly, areas where multilateral trade rules exist but fair international competition is hindered by high barriers and state support; and secondly, areas where trade rule-making has not kept pace with changes in the global economy. These “gaps in the rulebook” underscore the urgent need for reform and modernization of the World Trade Organization (WTO), particularly in its monitoring, transparency, and negotiating functions. (4)

As a result, three major threats to the global trade system are leading to heightened tensions and a looming threat of deglobalization, poised to significantly impact global trade in both the near and distant future.

1- The rise of protectionism:

The rise of protectionism gained significant momentum in early 2018 with the emergence of China as a global economic powerhouse. The Trump administration launched the ‘America First’ policy to reindustrialize the country and ensure America leads in strategic sectors. This policy included major protectionist shifts, such as imposing tariffs on Chinese goods worth hundreds of billions of dollars, aiming to curb what it labeled as China’s unfair trade practices and reduce the trade deficit. While the Biden administration’s trade policy is more sophisticated and less controversial, it does not reverse the core elements of ‘America First.’ Biden’s flagship industrial initiatives, such as the CHIPS and Science Act and the Inflation Reduction Act, go beyond that by including generous subsidy schemes for companies that manufacture in the U.S. or build infrastructure using U.S. materials. (5)

This approach has elicited significant reactions, with China retaliating by imposing tariffs on American exports, exacerbating the trade conflict. This tit-for-tat escalation led both nations to adopt additional measures, often citing national security concerns as justification to protect their domestic industries and reduce dependency on each other, further deepening the divide.

Chronological List of Key US-China Trade Disputes: (6)

U.S. Protectionist Measures:

2018

- March: President Trump announced steel and aluminum tariffs on imports from all countries, including China, citing national security concerns.

- June: The White House declared it would impose a 25% tariff on $50 billion of Chinese goods with “industrially significant technology,” effective from August 23.

- September: The U.S. announced a 10% tariff on $200 billion worth of Chinese goods, which would begin on September 24.

2019

- May: President Trump signed Executive Order 13873, placing Huawei on the Department of Commerce’s Entity List. This move banned Huawei from purchasing vital parts and components from U.S. companies without special approval and effectively barred its equipment from U.S. telecom networks on national security grounds.

- October: The U.S. Department of Commerce added 20 Chinese public security bureaus and eight high-tech companies, including Hikvision, SenseTime, and Megvii, to the Export Administration Regulations Entity List.

2020

- December: The U.S. Commerce Department imposed restrictions on China’s largest chipmaker, Semiconductor Manufacturing International Corporation (SMIC), citing an “unacceptable risk” that equipment supplied to SMIC could potentially be used for military purposes. Suppliers were barred from exporting the chip without a license.

2024

- February: The Biden administration doubled tariffs on solar cells imported from China and more than tripled tariffs on lithium-ion electric vehicle batteries imported from China. It also increased tariffs on imports of Chinese steel, aluminum, and medical equipment.

- April: The U.S. House of Representatives voted on a bill forcing Chinese company Bytedance to sell TikTok to a friendly buyer or face a ban in the U.S. within 180 days.

- May: Tariffs on imported Chinese EVs will rise to 102.5% this year, up from total levels of 27.5%. (17)

China’s Response:

2018

- March: In response to the U.S. tariffs, China imposed tariffs on 128 American products, including aluminum, airplanes, cars, pork, and soybeans.

- China has doubled down on its “Made in China 2025” strategy, aiming to achieve self-sufficiency in key technological sectors.

- The Chinese government has increased support for domestic industries through subsidies, state-backed loans, and investment in research and development.

2019

- May: China announced it would raise tariffs on $60 billion worth of U.S. goods.

- August: The Chinese Ministry of Finance declared new rounds of retaliatory tariffs on $75 billion worth of U.S. goods, effective beginning September 1.

2023

- July: Export controls on critical minerals, such as Gallium, germanium elements essential for high-tech industries, have been tightened, leveraging China’s dominance in these markets as a strategic tool.

2- Friend-shoring: also known as ally-shoring, involves relocating production and supply chains from potentially hostile or unstable regions to countries considered allies or friendly nations. This strategy seeks to reduce dependence on geopolitical rivals and ensure greater security and stability in supply chains. The concept has gained traction as nations increasingly view economic interdependence with geopolitical rivals as a vulnerability. The practice of friend-shoring reflects the growing influence of geopolitical tensions on trade relations. While this strategy offers significant benefits in terms of security, stability, and strengthened alliances, it also comes with notable costs, including:

- Increased expenses and supply chain complexity: supply chains require significant logistical adjustments while establishing new relationships, negotiating contracts, and setting up infrastructure in new regions which can be complex and time-consuming, potentially disrupting operations during the transition period.

- Economic Inefficiency: By leading to economic inefficiencies as companies move away from the most cost-effective production locations while trying to create a new eco-system in the hosting country. This shift can result in higher prices for consumers and reduced competitiveness for businesses on the global stage.

- Limited Supplier Options: Restricting supply chains to allied nations may limit the pool of available suppliers. This limitation can reduce competition, potentially leading to higher costs and decreased innovation in the long term.

Moreover, the International Monetary Fund (IMF) has raised concerns about a phenomenon known as ‘friendshoring’ warning that geopolitical tension is reshaping global foreign direct investment (FDI). A trend where FDI flows are increasingly directed toward geopolitically aligned countries rather than geographically proximate ones. The IMF also revealed that emerging markets and developing countries are particularly vulnerable to these shifting FDI patterns. These regions often rely more heavily on investment flows from geopolitically distant countries. The trend towards friend-shoring is expected to persist, with 73% of executives surveyed by management consultancy Kearney predicting an increase in this practice by 2026. (8)

3- The Global Race to Subsidize Industries: This surge in government support, aimed at boosting domestic industries and securing competitive advantages, has sparked intense debate about the potential benefits and pitfalls of such policies. As the United States, China, Japan, Australia, and other nations ramp up their industrial subsidies, concerns are mounting about the long-term implications for global Trade. The rise in government support across various industrial sectors is not adequately addressed by current WTO rules on industrial subsidies, leading to a lack of comprehensive regulations that fail to ensure a level playing field and fair competition. The rationale is clear: by providing financial support, the U.S. aims to reduce dependency on foreign supply chains, create jobs, and maintain technological leadership. China, on the other hand, has long been criticized for its extensive use of industrial subsidies. While subsidies can provide short-term benefits and bolster strategic industries, the risks of market distortion, fiscal strain, and trade conflicts are significant.

As countries navigate this complex landscape, international cooperation and prudent policymaking will be essential to ensure that the race to subsidize does not lead to a race to the bottom. Furthermore, Chinese state-owned enterprises (SOEs) benefit significantly from the decentralization of state equity and indirect control, which provides them with various advantages. These benefits include preferential domestic treatment, access to cheap finance (including from commercial lenders perceiving an implicit government guarantee), and the internationalization of their operations. This strategic positioning allows Chinese SOEs to expand their global footprint and maintain a competitive edge in international markets. These advantages have led to numerous complaints filed with the WTO, calling for action to maintain a healthy competitive environment. (9)

Moreover, The United States Trade Representative’s annual report claims that China is damaging global industries through massive domestic subsidies. China challenged this statement in the World Trade Organization, pointing to the large subsidies the United States has provided under the Inflation Reduction Act and the CHIPS and Science Act. As countries around the world follow suit and offer substantial industrial subsidies, globalization may be on the brink of reversal risking damage to global productivity and growth. (10)

An Analysis Simulating a Complete Decoupling Scenario between the U.S. and China:

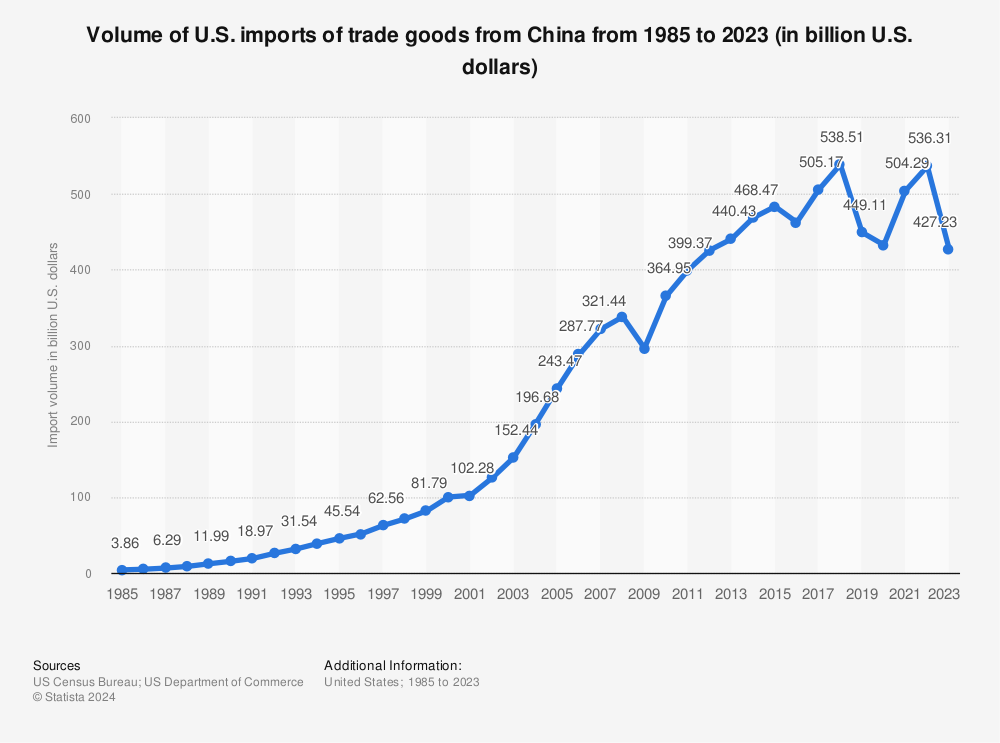

After four decades of economic engagement between the U.S. and China, attempting to decouple this extensive relationship overnight would lead to counterproductive economic hardship. As of 2023, the total value of U.S. trade in goods with China reached approximately $575 billion in two-way trade. This figure comprised an export value of $147.8 billion and an import value of $427.2 billion. Identifying the real consequences and costs of decoupling is essential for policymakers to make informed decisions before engaging in a trade war that could irreparably damage the current global trading system. (11) In a recent Finance and Development (F&D) article, IMF economists Marijn Bolhius, Jiaqian Chen, and Benjamin Kett estimate that a hypothetical geoeconomic fragmentation scenario could lead to a permanent loss of 2.3% in global GDP. “The most worrying downside risk of fragmentation in global trade is a further escalation of current tensions to the extent that countries could start to form blocs that stop trading with other countries and force third parties to choose sides,” explain the IMF economists. Under this scenario, low-income countries would suffer the most, experiencing a permanent GDP loss of more than 4%. The IMF economists warn that these countries and emerging markets “would get caught in the crossfire,” losing access to essential imports and export markets. Even under a less severe “strategic decoupling” scenario, global output is estimated to permanently shrink by 0.3%. This scenario involves heightened sanctions and trade policies, resulting in the elimination of trade in high-tech sectors between China and the U.S. (12)

In the same vein, a study by the U.S. Chamber of Commerce in 2021 highlighted key findings on the aggregate costs of decoupling the U.S. economy from China:

- Trade Channel Impact: If 25% tariffs were expanded to cover all two-way trade, the U.S. would forgo $190 billion in GDP annually by 2025.

- Lost Market Access: The loss of U.S. market access in China today would result in revenue and job losses, diminished economies of scale, smaller research and development (R&D) budgets, and reduced competitiveness.

- Investment Impact: In a scenario where half of the U.S. foreign direct investment stock in China is sold off, the U.S. stands to lose $25 billion annually in capital gains. Additionally, this scenario could result in projected GDP losses of up to $500 billion.

- People Flows: If future flows are reduced by half, it could lead to a loss ranging between $15 billion and $30 billion per year in services trade exports for the U.S.

- Idea Flows: A complete decoupling would undermine productivity and innovation, leading to reduced attraction for venture capital investment in U.S. innovation initiatives.

Moreover, concerning the impact of decoupling on industry-level costs, the study revealed significant ramifications that could diminish U.S. competitiveness:

- Aviation Industry: Decoupling could result in annual losses estimated between $38 billion and $51 billion for the U.S. aviation sector. Notably, market share losses could accumulate to $875 billion by 2038 due to reduced aircraft sales, leading to lower manufacturing output, declining revenues, and job losses in the U.S.

- Semiconductor Industry: In a decoupling scenario, China’s pursuit of self-sufficiency in the semiconductor sector could cost the U.S. industry between $54 billion and $124 billion in lost output. This risk could jeopardize over 100,000 jobs, $12 billion in research and development (R&D) spending, and $13 billion in capital expenditure.

- Chemicals Industry: Decoupling would entail losses from tariff impositions alone, ranging from $10.2 billion in reduced U.S. output and 26,000 lost jobs to over $38 billion in output losses and nearly 100,000 lost jobs for the U.S. chemicals industry.

- Medical Devices Industry: Decoupling would lead to abandoned market share in China, resulting in a net U.S. loss of market share valued at $23.6 billion in annual revenue. This translates to lost revenue exceeding $479 billion over a decade. Additionally, the costs of reshoring supply chains and restricting product and intermediate input imports from China, coupled with potential retaliation against U.S. exports by Beijing, would further compound the challenges faced by the U.S. medical devices sector. (13)

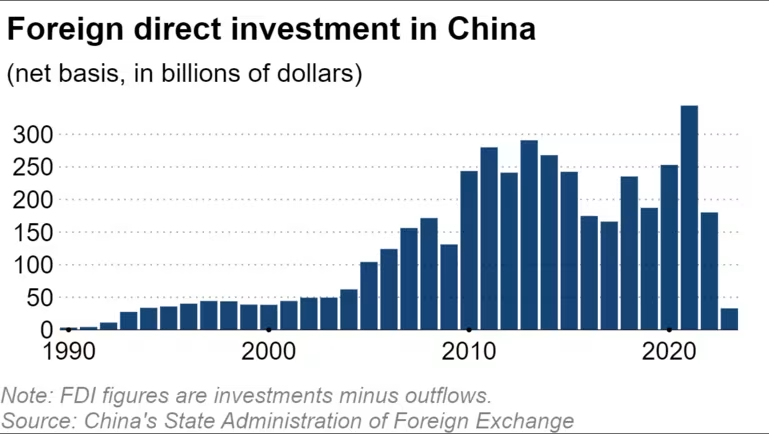

The flow of foreign direct investment in China: (14)

Conclusion:

The rivalry between the United States and China has become one of the defining geopolitical dynamics of the 21st century, with far-reaching implications for global trade and economic relations. As the world’s two largest economies, their competition spans various fronts, including technology, military dominance, and ideological influence. At the heart of this rivalry lies a struggle for economic supremacy, with both nations vying for dominance in key industries and markets.

The future of trade between the U.S. and China will likely be shaped by a combination of cooperation and competition. While efforts to negotiate trade agreements and resolve disputes through diplomatic channels may offer avenues for cooperation, underlying geopolitical tensions and strategic interests will continue to influence trade dynamics. Moreover, the emergence of new technologies such as artificial intelligence, quantum computing, and 5G networks will further complicate the landscape, as both nations vie for leadership in these critical sectors.

In this context, the future actions of both rivals are hard to predict, but any further escalation of trade disputes would significantly impact global trade. Additionally, protectionist tendencies and growing trade disputes will only lead to uncertainties in financial markets, and prompt capital outflows from various regions worldwide. Higher tariff barriers would lead to increased prices and a weakening of currencies, causing substantial inflationary pressures. These protectionist measures may also reduce technological spillovers in the global economy and accelerate the deglobalization of trade and information, reversing many of the gains countries have enjoyed over the last four decades. (15)

As the rivalry intensifies, countries around the world will need to navigate carefully to avoid being caught in the crossfire while also seizing opportunities for collaboration and mutual benefit. Ultimately, the future of trade will be marked by the shifting balance of power and influence projected by both rivals, with implications for global economic growth, supply chain resilience, and geopolitical stability. The evolving geopolitical landscape will require nations to adapt and forge new pathways for cooperation and economic prosperity, ensuring that they can respond to challenges and leverage emerging opportunities effectively.

References: